Can I Retire Early?

The pandemic has been a trying time for most of us. Our normal daily routines have been disrupted, giving way to new ways of living. We have had to adapt and change to new habits and lifestyles. I frequently hear that the pandemic has provided many of us with a new perspective as to what really matters in life. One aspect of this is that people are reassessing their priorities and re-thinking their views on life, health and family.

Many people are asking,“Can I retire early?”

As wonderful as this sounds, there are some important considerations to think about before pulling the trigger. This article aims to highlight some things you should consider before deciding to retire early.

The Income Gap

Unless you have a pension available to you from your employer, Social Security is likely to be your main source of steady income in retirement. The earliest age that you can collect your benefit is 62. The benefit will increase for each year that you wait, with the maximum benefit coming if you wait until age 70 to claim. The difference between claiming at age 62 and age 70 is roughly a 70% increase in your initial benefit.

There are, of course, other factors that come into play including whether you have any earned income from working or self-employment, your health and your spouse’s situation if you are married.

Regardless of when you decide to collect your benefit, if you retire early, you may find yourself without a steady income stream for several years.

One investment vehicle people often turn to is annuities. While annuities can have a negative reputation, they are good for creating an income floor or a steady stream of income that people can count on. The annuity can provide a safe and predictable income stream. This can be a good way to replace your paycheck. Essentially, an annuity is the process of transferring investment risk from yourself to an insurance company in exchange for a steady stream of income.

This solution does not work for everyone however and there are other strategies that can be used for the person who does not want to surrender their assets to an insurance carrier. It is also important to shop around for an annuity that offers a solid income stream, no or minimal surrender costs and one that has relatively low expenses.

The Bucket Approach

Much has been written about the bucket strategy. This is the process of allocating your assets in such a way that the most conservative investments are positioned to be consumed in the first 5 years of retirement and the more aggressive investments are positioned to grow and be consumed later in your life (potentially 20-30 years down the road). This can be an effective way to approach creating a retirement income stream that rises over time.

How does it work?

First, you need to decide how much income you need to meet your basic needs plus the additional money for the lifestyle you desire. It all starts with creating a good budget. If sitting down to pencil out your spending does not sound like fun, you can breathe a sigh of relief because there are some great technology solutions that help you to track your spending. And if you cannot find one, feel free to contact our office as we can give you a wonderful tool to help you track your expenses.

After getting clarity on how much your ideal lifestyle will cost you need to also consider inflation. This is the process by which everything you buy and do will get more expensive as you age. For a great article on inflationCLICK HERE

After solving for how much your desired lifestyle will cost and how much inflation will increase it you need to solve for how much money you need to spend in the first 5 years of retirement. Once you do this you then strategically position your assets correctly by putting the first 5 years of spending in the safest assets possible. Examples include short-term treasuries, high quality corporate bonds, high quality municipal bonds to name a few. These investments will not grow much but will be there when you need them most.

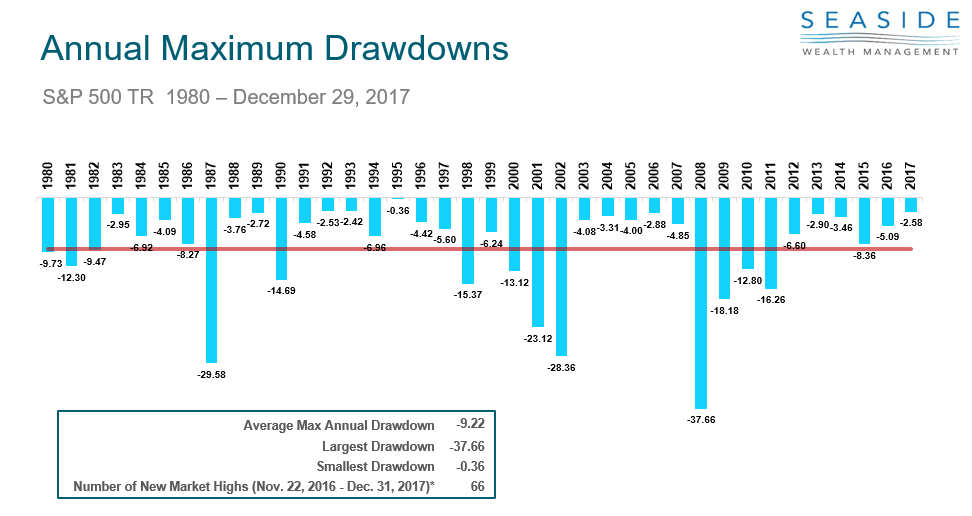

The stock market can help you create a rising income stream but it can be very volatile as well (click here to read more). Since 1980 the average intra year decline of the S&P 500 is 14%. In other words, you should expect the stock market to decline about 14% at some point every single year.

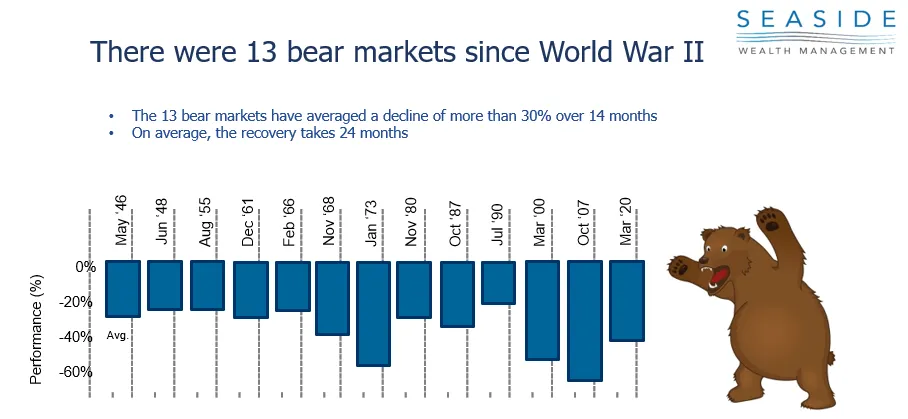

About every 5-10 years the market goes down by 20% or more.

If all of your money was in the stock market and went down by 20% you would not want to sell shares of great companies at fire sale prices in order to fund your lifestyle. In fact, market volatility is what helps you to build wealth while working by dollar cost averaging and purchasing shares at discounted prices. Now that you are retired, this is the last thing you want to do!

Once you solve for the amount of income you need in the first 5 years and put that amount of capital into safe investments you must determine how much you need to spend in years 6-15 of retirement as well as years 15-30 and beyond. You then select appropriate investments for those specific time horizons and invest the portfolio accordingly.

The 1– year bucket might hold relatively safe investments like money market funds, bonds, bond ladders, CDs and other similar vehicles. For example, your spending and consumption needs for years 6-15 can be placed in high quality, dividend paying investments that will grow and also create income to live on.

For your retirement spending needs in years 16-30 and beyond you need significant growth to keep up with the ravages of inflation. Asset classes like small cap (owning small companies), small cap value, international small cap and emerging markets are wonderful ways to grow your capital to meet increased spending needs in the future.

It’s important to recognize that the strategies you used to accumulate wealth are completely different from the strategies you need to use to decumulate your assets. The rules of the game change when you enter retirement! Retirement income planning is a specialty planning niche.

Other consideration- health insurance

If you are going to retire early you need to consider how you will handle your health insurance needs. If you received your health insurance through your employer this is going to be an expense to add into your budget. Medicare doesn’t begin until age 65. For every year you retire before 65 you need to purchase medical insurance. There are many options on the private market and we can introduce you to experts in this field to help you make a good choice. That being said, you can easily plan to spend $1,000 per month per person on medical insurance. While there are certainly less expensive options out there, we routinely see $12,000-$15,000 per person annually.

One option might be to continue your health insurance from your old employer via COBRA. While the coverage will be the same as when you were employed, the cost will be significantly higher as your employer is allowed to pass on the full cost of coverage to you. In some cases this may still serve as a reasonable bridge until Medicare kicks in.

Once you go on Medicare there will still be expenses (click here for more information). While Medicare Part A is free, you will pay for Part B. If you are collecting Social Security the cost of Part B is deducted from your Social Security check. In 2021 the cost of Medicare Part B starts out at $148.50 and gets more expensive depending on your Modified Adjusted Gross Income. Failing to take the costs of healthcare into consideration is a major mistake we see early retirees make.

What are you going to do with yourself if you retire early?

Another often overlooked but equally important thing to consider is what are you going to do with yourself if you are not working? For many, the thought of having every day be like Saturday is exciting, especially if you are tired from feeling the grind at work. However, you may be surprised that having every day off is not always what it’s cracked up to be. We recommend spending some time contemplating what you want to do with your time in retirement. Early retirees often express a lack of purpose and meaning in their lives once work is done. In fact, we like to give our retirees some material to read in order to help them navigate this new season in their lives:

You may be thinking that spending your days pursuing leisurely activities like reading, travelling, and gardening sounds great about now! But you may be surprised to learn that this is not always the case (click here to read more).

What is becoming increasingly clear is that retirees need meaning, purpose and passion in their lives in order to feel fulfilled. Before you leave the workforce, make sure to give careful consideration to what gives you a sense of purpose in your life. It’s important to think these things through before you retire rather than during retirement!

For more details on this subject or if you would like to discuss it further, please feel free to contact our office at your convenience.

Read More

How Social Security Timing Can Make A $600K Difference in Taxes

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

Smart Money Moves to Make for 2026

26 Things To Consider In 2026