How to not run out of money in retirement

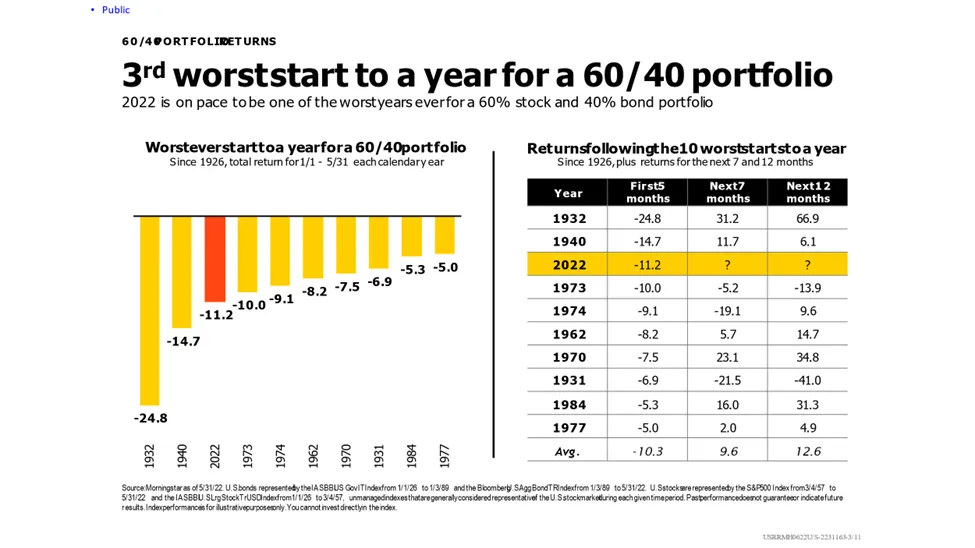

Retirees are living longer and enjoying many years of good health after they are done working. The average life expectancy of someone age 65 is into their mid-80’s with a high probability of making it into their 90’s. With inflation as high as it’s been in 40 years you may be wondering about how long your money will last. Couple that with the current market volatility you may be concerned about how you can make sure to not run out of money in retirement. One example of the severity of the current market volatility is the fact that this is the third worst start to a 60/40 portfolio on record. While the 60/40 portfolio is not necessarily the optimal investing strategy, this is a balanced investing allocation between stocks and bonds. Both asset classes have been impacted during this period high inflation and rising interest rates that has affected the stock market so far in 2022.

Many retirees are facing the possibility of being retired for 30 years or longer. In some cases, their retirement may be longer than their working career! It’s critical that your financial resources are managed wisely so you do not outlive your assets. In addition, inflation has reared its ugly head increasing the cost of everything you purchase.

Ways to increase income in retirement

The easiest way to increase income in retirement is to delay taking your Social Security benefit. Many Americans take their Social Security benefit at the earliest age possible which is 62. If you choose to delay your benefit it increases at 8% per year for every year you delay. Click here for more information

Depending on your birthday, delaying Social Security until age 70 can result in nearly a 70% increase in your benefit amount. Additionally, your Social Security benefit receives cost of living adjustments. Having a larger benefit gives you more money that is receiving increases from COLAs each year.

Consider purchasing rental properties

Investment properties offer a steady income stream that is diversified from the stock market. Real estate can be a nice hedge against inflation because the rents tend to adjust upwards over time. Like Social Security, rental income has built in levers to adjust for inflation. Oftentimes leases are signed with agreed upon rent increases over time. In this way, rental property can also contribute to creating a rising income stream throughout retirement.

With the rise in real estate prices over the last two years, the timing of this strategy might not be ideal today. However, as a result of inflation, the Federal Reserve is increasing interest rates. This may have the effect of slowing down the housing market and many are predicting a decline in prices. If prices fall to more attractive levels, this may prove to be a buying opportunity for real estate in the future.

What about the rising cost of medical care?

With medical costs spiraling out of control, many people are paying a significant amount of money towards their health insurance as they age. Today, many people are purchasing Qualified Longevity Annuity Contracts or QLACs to help combat this. A QLAC is a deferred annuity that provides guaranteed payments for life.

The payments are guaranteed by the insurance company, and they are not affected by volatility in the stock market.

The beauty of the QLAC is you can use funds in your IRA or tax-deferred retirement vehicle which will not subject them to Required Minimum Distributions. In other words, the QLAC will help you reduce your tax bill in retirement by keeping RMD’s lower, although income from a QLAC is taxable and subject to RMDs once you start taking it. You will purchase the annuity and then take the income as annuity payments at a later age. This income will last as long as you do. Essentially, the QLAC can be looked at as longevity insurance. Click here to learn more.

Create a Budget

Financial experts agree there’s no way to make your money stretch if you don’t know your income and expenses. Most people don’t have a clue about how much they spend in a month or a year. Having a firm handle of what you spend is a great way to gain clarity. I recommend reviewing it at least on an annual basis and adjust it as needed.

Get a Part-Time Job

Now that you are retired you can work that job you always wanted but were afraid you couldn’t afford to. Whether it’s being a starter at the golf course or working at the local library, having a part-time job can provide some added income each month. You can also consider doing consulting work in your professional field. In addition, there are many social benefits to keeping yourself employed which can do wonders for your overall wellbeing.

Use the right withdrawal rate:

Historically, taking 4% of your portfolio out per year has led to positive results over time. This limits the amount of money that comes out of your portfolio each year. During down years, your distributions might get smaller. During strong years, your distributions can increase. Being systematic and disciplined with your withdrawal strategy can make all the difference in your portfolio lasting as long as it needs to.

Avoid Making Large withdrawals during a down market

This is a good time to scale back spending on large purchases if possible. Taking a large distribution during a down period in the markets can compound the impact of this market decline on your future spending power. We all know we should be “buying low and selling high” when it comes to our stock market investments. Taking a large distribution during a down market year has the reverse effect of selling low. Try to hold off on taking large distributions until markets recover.

The Good News

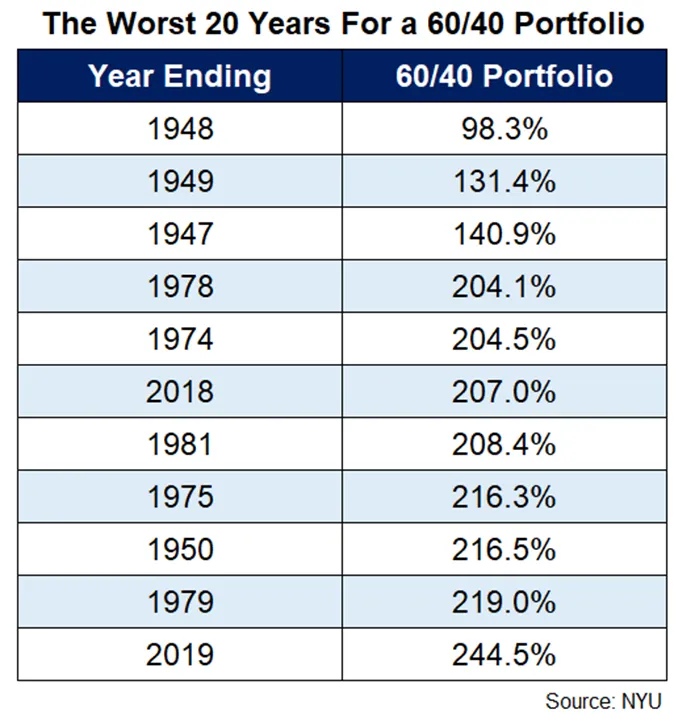

Looking at the 60/40 portfolio, the good news is the rough starts in the markets won’t last forever. History shows us that declines tend to lead to periods of excellent performance over time. Even the worst 20-year period had some pretty strong results.

Given the negative headlines and sentiment it’s easy to succumb to emotion and make investing decisions that will impact your long-term financial security. With history as our guide, the best course of action is to rebalance, invest extra cash if you have it and maintain the discipline of your investing strategy.

Please give us a call if you have concerns or would like to discuss further.

Read More

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

How Often Should I Meet With My Financial Advisor?

Smart Money Moves to Make for 2026

26 Things To Consider In 2026