Inflation – What You Need To Know

There is much speculation among financial experts that inflation is going to rear its ugly head in the near future.

Inflation is the scenario in which most things we purchase get more expensive over time. This can be devastating as your retirement savings don’t go as far as you had planned. Without proper planning, inflation can ravage an otherwise healthy retirement lifestyle. Inflation is also known as the silent killer. Failing to effectively plan for inflation is one of the top three financial planning mistakes that we see in our practice

Historically, the general rule of thumb in the financial planning community was to use an assumption of 3% for an annual inflation rate. Over the last 20 years however, inflation has been relatively tame. For the current Consumer Price Index click here. During the financial crisis of 2008 the biggest concern was actually that we would enter into a deflationary environment! The Federal Reserve did everything they could to buoy asset prices in order to avoid this scenario. In fact, the 20-year inflation rate is currently running right around 2.3%.

With all of the federal spending and stimulus programs that have been put in place over the last 15 months there is much concern that inflation is going to come back with a vengeance. Another driver of inflation is the economic reopening of America fueled by more people getting vaccinated, which may cause upward price pressure in industries that lagged behind during the pandemic.

The media has been steadily beating the drum that inflation is something you should be concerned about, and they are correct in highlighting this as an area of concern.

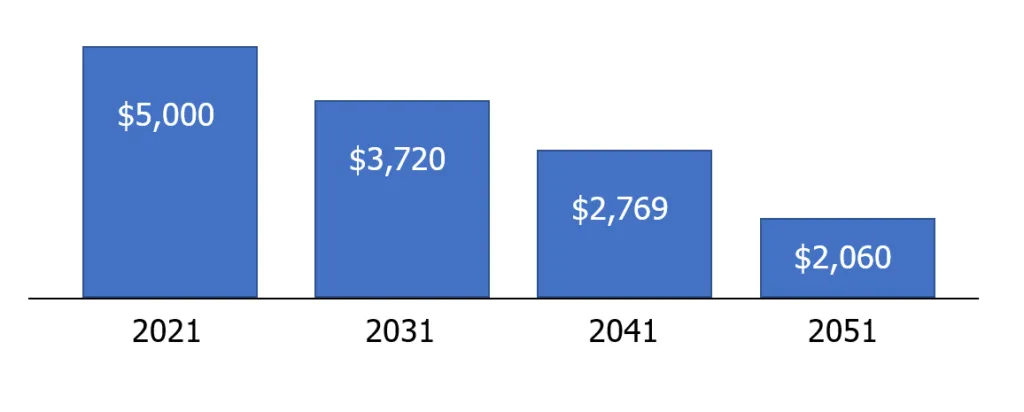

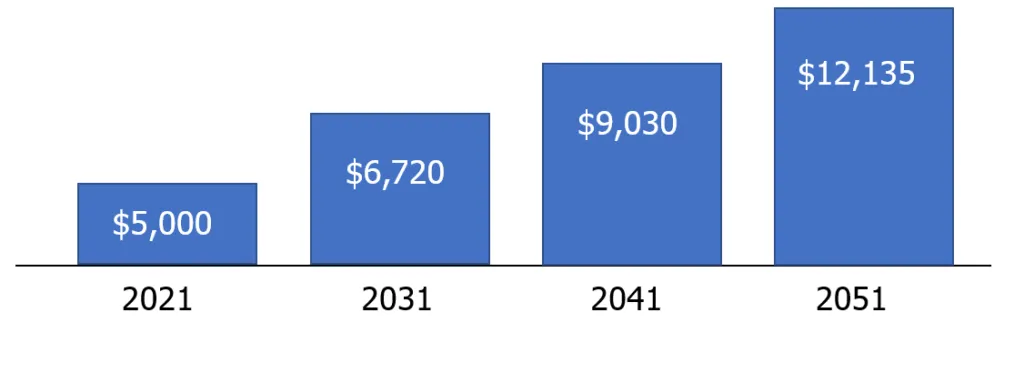

The reason why inflation is so devastating to retirees is because it slowly erodes the purchasing power of your retirement nest egg. Take a look at the graph below to show the decrease in your purchasing power if you aren’t prepared to deal with it.

People are living 30 or more years into retirement and decline purchasing power can be a sad reality for some. Another way to view it is to ask yourself “what type of return on my savings must I earn to keep up with inflation?”. The chart below shows that $5,000 today must actually grow to $12,135 in 30 years to give you the same purchasing power that $5,000 today gives you.

This can be a daunting concept for some when you think about how to maintain your purchasing power over the course of your retirement years.

Knowing that inflation is on the horizon is one thing, knowing what to do about it is another.

What should you do about inflation?

People have asked whether they should invest in real estate, hard assets like gold or even cryptocurrency to combat the insidious effects of inflation. While all of these asset classes are worthy of consideration there is another asset class that remains king of the hill in conquering the impact of inflation. Owning shares of the greatest companies in the world has proven to be the best hedge against inflation out there.

In the most recent Ibbotson data (1926-2020), the average annual compound return of the S&P 500 was just over 10%; CPI inflation has compounded at just less than three percent. Thus, the mainstream equity investor increased their purchasing power at quite a bit more than twice the rate at which inflation has clawed it back.

The best part about this is you don’t have to do anything but remain invested! The great companies of the world did it for you! By passing on the cost of inflation to their consumers, the companies you owned were handily keeping up with the rising cost of goods and services. Keep in mind, this isn’t a perfect process. Sometimes inflation will leap ahead before companies can catch up and eventually adjust. Share prices may take some time to reflect that companies are keeping up with inflation. Nonetheless, if you give it enough time, the great companies of the world do a terrific job of outpacing inflation.

Think about it.

Will you stop buying toilet paper and toothpaste or putting gas in your car simply because the prices have gone up? The overwhelming evidence over long time horizons is that leading companies have the pricing power to pass on increased costs to the consumer. But it gets even better! Great companies also wage war against rising costs by innovating and becoming more productive. And innovation is what America does best.

Will inflation get really bad?

Even if we see a prolonged period of inflation, equity investors shouldn’t be concerned. During our country’s last bout with inflation the S&P 500 stood at 96 in 1967 and as I write, it’s above 4,100—70 times higher. The dividend that year was $1.98; it’s running at a rate close to $60 this year—up 30 times. The Consumer Price Index ended 1960 just under 30; last month it came in at 267—nine times higher.

Here’s a link to the chart of S&P 500 earnings and dividends prepared annually by Dr. Aswath Damodaran, professor at NYU’s prestigious Stern School of Business.

It’s worth a look. Forget the fact that the S&P 500 has increased almost 65 times in 60 years. Forget that earnings have increased from $3.10 in 1960 to $138.12 last year. Pay attention to the fact that the cash dividend of the S&P 500 grew at a compound growth rate of 5.8%. If a rising retirement income is what we want it’s hard to beat the dividend stream of the greatest companies in the world.

Want more tips on how to be a successful long term investor? Click here!

And if you are still concerned, another great exercise you can do is review your expenses. There are so many things in life that are out of our control, but managing a budget is something within our control. There are some wonderful tools to help you do this and if you want to learn more please give our office a call.

Additionally, if inflation has got you concerned please feel free to reach out and we can schedule some time to talk about your situation.

Read More

How To Protect Your Retirement Savings From A Market Crash

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

Smart Money Moves to Make for 2026

26 Things To Consider In 2026