Long-Term Investing: The Key to a Successful Retirement

Being a successful long-term investor is easy as long as you keep these key takeaways into consideration:

- Be patient and remain calm in all market environments (we take each scenario into account when building your asset allocation).

- Your retirement time horizon could be 40+ years, so you do have the time to weather through the storm.

- Being aware of tax consequences or tax advantages can keep your plan on track.

- Diversification helps reduce volatility.

- Give your portfolio the time it needs to grow.

- Periodically review your risk tolerance and make changes based upon your goals, not emotions.

Investing, in general, is the act of allocating resources, usually money, with the expectation of generating an income or profit. You can invest in endeavors, such as using money to start a business, in assets like stocks or bonds, or in real estate in hopes of reselling it later at a higher price.

Being an investor means different things to different people. One type of investor is the short-term investor. This simply means you are purchasing financial instruments intended to be held for less than one fiscal year. This type of investing can come with significant positive gains. But is it really worth the increased speculation, possible tax consequences, and potential high transaction costs?

Another type of investor is the long-term investor which is someone who intends to hold a security, portfolio, or investment strategy for a term of longer than one year with a specific goal in mind such as funding retirement. What I would like to do is discuss what it looks like to be a successful long-term investor, and some of the things you can implement in order to make your financial plan come to life. Currently Seaside Wealth Management is planning for retirement to last 20, 30, or even up to 40+ years. Warren Buffet once said:

“if you aren’t thinking about owning a stock for 10 years, don’t even think about owning it for 10 minutes.”

We believe that investing should be approached with a long-term vision and goals. This leads us to Our Principles:

- We have faith in the future

- We have patience

- We have discipline

It may sound easy for you to stay the course and be a successful long-term investor. Here are some tips to keep in mind on your journey to and through retirement: The first thing if you are wanting to continue to be a long-term successful investor would be to remain calm during all market cycles. We all know that in the short-term we can expect the financial markets to be up and down, and these movements can be very stressful. What many people, not working with advisors, do is sell their assets to protect from losing more. This is just locking in their losses and they could potentially miss out on some of the best market days. Historically, the market always comes back and only takes an average of two years to recover.

For more information about market volatility, pleaseclick here to look at one of our recent blog posts.

You may be thinking, “I am about to retire”, “I’m in retirement already”, or “I don’t have the time horizon to have my portfolio weather through that type of market storm”. You’re not alone! A lot of people in your same situation are thinking the same thing. Keep in mind with an average retirement of 30 years that we actually do have a time horizon long enough to make it through. Also, with the proper asset allocation and diversification we can help with some of the volatility.

When it comes to investing and financial planning another thing to consider as a successful long-term investor would be to be conscious of tax ramifications. As the current law sits if you hold investments for one year and a day you are entitled to the more favorable long-term capital gains rates. In 2021 if you are married filing jointly and have taxable income of $80,800 or less your capital gains tax rate would be 0%. If your household income is $80,800-$501,600 then you would have a capital gains rate of 15%. If your household income is above $501,600 then your tax rate would be 20%. These are substantially lower than your ordinary income tax brackets so by saving money on taxes as a long-term investor can help allocate more assets towards your retirement.

Here is a chart to clearly show which capital gains rates you would currently be exposed to if you hold your assets for the long-term. Click here to view on the IRS website.

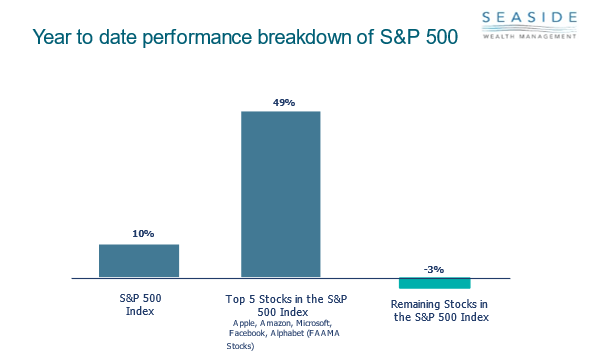

If you are taking the route of the short-term investor, you might be investing in individual stocks to help turn a quick profit. This is great, but near impossible to consistently do over time. If you look at this graph you can see the S&P 500 during this period was up 10%. If we look under the hood only five stocks out of 500 were up and 495 were down.

This can also lead to more negatives than positives. If you decide to realize the short-term gains, now your gains are taxed at ordinary income rates instead of the more favorable capital gains rates. Also, what happens if you pick the wrong stock and you end up losing your entire investment? A long-term successful investor will most likely use mutual funds or exchange traded funds (ETFs). These are both baskets of securities to help diversify away the concentration risk and mitigate some of the tax consequences.

With that said here are Our Convictions:

- We believe that markets are efficient

- We do not believe in market timing

- We do not change asset allocation unless your specific goals have changed

- We do not buy individual stocks

- We hold fast to our standards

- We believe that behavior is the critical variable that can be controlled

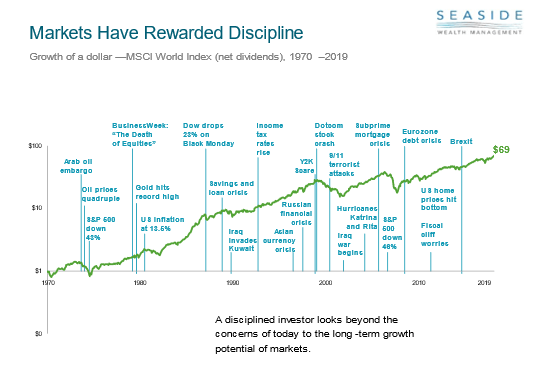

To piggy back on some of the points above as a short-term investor you are forced to pay attention to the day-to-day movement, or the next “black swan” event. Here is a chart that shows how the markets have rewarded discipline through different macroeconomic events.

As a successful long-term investor, you actually want to do the opposite and give your plan and investment portfolio a break. What I mean by this is that you’ve committed for a number of years to see the wonderful more predictable investment results so give your plan the time it needs to grow. Checking your investment returns each day, like mentioned before, will only cause you to act on emotion. It may sound crazy, but one small mistake over a 30-year period could derail your entire financial plan. Let’s continue to be patient, and watch how the eighth wonder of the world, compound interest, works in your favor.

Finally, while being a successful long-term investor it’s a great idea to review your risk tolerance from time to time. Let’s not mistake this with market timing, and making changes to your investment portfolio because of the noise we are hearing on the news, or what we think is going on in the economy. The rational reason to make a change to your investment portfolio would be because your goals have changed.

This can help you determine if you need to make a change, Our Process:

- Your values help to define your goals

- The goals dictate the plan

- The plan dictates the asset allocation

- The asset allocation dictates diversification into the right kinds of investments

If you would like to discuss this topic in more detail, or have any other planning or investment related questions, please reach out to our team at Seaside. We would welcome the conversation.

Read More

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

Smart Money Moves to Make for 2026

26 Things To Consider In 2026

Smart Year-End Money Moves to Strengthen Your Financial Future