Secure Act 2.0: Everything You Need To Know About

After a multi-year journey, the Secure Act 2.0 is now law. And it's packed with tax and retirement planning changes you need to know about.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act, passed in December 2019, brought a wide range of changes to the retirement planning landscape, from the death of the ‘stretch’ IRA to raising the age for Required Minimum Distributions (RMDs) to 72. Nearly three years to the day after the passage of the Secure Act, Congress has passed the Secure Act 2.0.

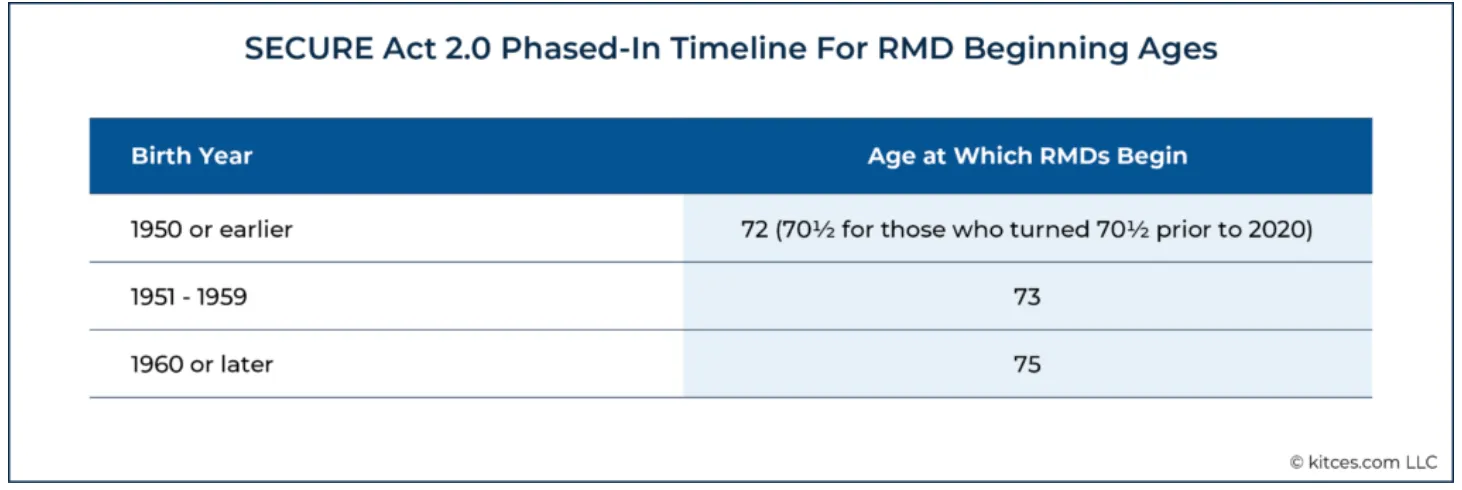

Changes to Required Minimum Distributions…….again.

The Secure Act 2.0 pushes Required Minimum Distributions (RMD’s) out to age 73 for people born between 1951 and 1959. For anyone born after 1960, RMD’s are pushed out to age 75!

In addition, the bill decreases the penalty for missed RMD’s from 50% to 25% of the shortfall, and if the mistake is corrected in a timely manner, the penalty is reduced to 10%.

Ultimately, pushing back the age for RMDs is a neutral-to-positive change for most people. For individuals who already need to take distributions beyond their RMD level to support living expenses, the change is largely irrelevant. For some of you, however, the change will be viewed as welcome news, as it may allow you to push off retirement-account income for a few more years in an effort to stave off higher Medicare Part B/D premiums and, perhaps, to have a few more years of tax-efficient Roth conversions.

Roth Related Changes

The Secure Act 2.0 includes a significant number of Roth-related changes (both involving Roth IRAs as well as Roth accounts in employer retirement plans). Most of these changes will allow us more planning opportunities for you and we view these as positive.

The Backdoor Roth IRA Contribution strategy lives on…… for now!

The Secure Act 2.0 does not eliminate the ability to contribute to a backdoor Roth IRA.

Elimination of RMD’s for Roth 401(k)’s

Starting in 2024, Roth accounts inside of employer sponsored retirement plans will no longer have Required Minimum Distributions. Currently, Roth IRA’s are not subjected to RMD’s but Roth 401(k)’s, Roth 403b’s and Roth 457B’s are subjected to RMD’s. This goes away in 2024.

Creation of Roth SIMPLE IRAs and Roth SEP IRAs

Beginning in 2023, business owners and consultants will have 2 new opportunities for Roth contributions. Now Simple and SEP IRA’s can have a Roth component. Previously, SIMPLE and SEP plans could only include pre-tax dollars.

Since this is such a new feature, it may take some time before the major custodians are prepared to establish these types of accounts.

Additional Employer Contributions eligible for Roth Treatment

Secure 2.0 allows the after-tax contributions to go into the Roth portion now. Employer matching contributions can now go into the Roth component of the 401k) which is a big change. These contributions will now be included in your income for the year.

High Wage earners are now required to use the Roth option for catch up contributions.

Secure 2.0 gives you more Roth options but in this example, the bill takes the tax decision out of your hands requiring high income earners to make catch up contributions to the Roth component of the 401k beginning in 2024. This is likely in an effort to increase revenue to help pay for other aspects of the legislation. The new rule applies to 401(k)’s, 403Bs, 457B but NOT to Roth IRA’s or Simple IRA’s. The income threshold where catch up contributions are required to go Roth is $145,000 and this will be adjusted for inflation in future years.

(Limited) 529-to-Roth IRA Transfers Allowed After 15 Years

Beginning in 2024, some people may be allowed to move 529 plan money directly to a Roth IRA. This is a great option but it comes with some stipulations:

- The Roth IRA receiving the funds must be in the name of the beneficiary of the 529 plan.

- The 529 plan must have been established for at least 15 years.

- Any contributions to the 529 plan within the last 5 years (and the earnings on those contributions) are ineligible to be moved to a Roth IRA;

- The annual limit for how much can be moved from a 529 plan to a Roth IRA is the IRA contribution limit for the year, less any 'regular' traditional IRA or Roth IRA contributions that are made for the year (in other words, no doubling up with funds from outside the 529 plan); and

- The maximum amount that can be moved from a 529 plan to a Roth IRA during an individual’s lifetime is $35,000.

This will allow the tax-advantaged nature of this money to remain intact for the beneficiary even if they don’t use if for higher educational expenses.

IRA Catch-Up Contributions to be Indexed For Inflation

IRA Catch up contributions were created in 2002 and used to be $500. This amount was increased to $1,000 in 2006. The catch-up contribution amount has always been a flat amount. Now it will be indexed for inflation and allowed to increase over time naturally. The increases will be in $100 increments so we will make sure to help you keep track of this!

Increased Plan Catch-Up Contributions for Participants in their early 60’s

Beginning in 2025, workers who are aged 60, 61, 62 and 63 can contribute more to their 401(k) plan. The catch-up contribution amount is increasing to $10,000 (indexed for inflation).

Similarly, SIMPLE IRA’s will have the catch up contribution amounts increased to $5,000 (indexed for inflation) beginning in 2025.

New Rules for Qualified Charitable Distributions (QCD’s)

The age at which you can make a QCD remains unchanged at 70.5. QCDs are a great way to benefit the charity of your choice while reducing your future RMDs and lowering your tax bill. There are however, two modifications to the QCD rules:

- Maximum Annual QCD Amount Indexed For Inflation. When the QCD provision was first introduced more than 15 years ago, the maximum annual QCD amount was limited to $100,000. Since then, the maximum amount has remained the same. Beginning in 2024, however, the QCD limit will change for the first time ever as it will be linked to inflation; an

- One-Time Opportunity To Use QCD To Fund A Split-Interest Entity. Beginning in 2023, taxpayers may take advantage of a one-time opportunity to use a QCD to fund a Charitable Remainder UniTrust (CRUT), Charitable Remainder Annuity Trust (CRAT), or Charitable Gift Annuity (CGA)

At first glance, the ability to fund a CRUT, CRAT, or CGA with a QCD may seem like a significant benefit for some IRA owners, since it essentially allows you to remove funds from a traditional IRA tax-free to pass on to future generations free of income or estate tax. However, the reality is that there are a lot of strings attached to the provision that make it not quite the deal it may appear to be at first, especially for those interested in using their IRAs to fund a CRUT or CRAT. More details to follow in the future.

Qualified Longevity Annuity Contracts (QLACs)

SECURE 2.0 increases the maximum amount that can be used to purchase QLACs to $200,000 (up from $145,000 in 2022 and what would have been $155,000 for 2023).

There are a number of new rules under Secure Act 2.0 for accessing retirement funds in times of need. These include:

- The age 50 exception has been included to include private sector firefighters.

- The age 50 exception has been expanded to include state and local corrections officers.

- The age 50 exception has been included to include qualifying workers with more than 25 years of service with a single employer.

- The permanent reinstatement of smaller qualified disaster distributions.

- The creation of exceptions for individuals with a terminal illness.

- The creation of a new emergency withdrawal exception.

- The creation of an new exemption for qualified long-term care distributions.

What’s not in the Bill?

SECURE Act 2.0 contains no provisions that:

- Limit the use of the Back-Door Roth or Mega-Back-Door Roth contributions;

- Place new limits on who can make Roth conversions;

- Create non-age-based RMDs (e.g., require balances in excess of a specified amount to be distributed);

- Change the age at which QCDs can be made (as it continues to be age 70 ½);

- Implement new restrictions on Qualified Small Business Stock (QSBS);

- Eliminate new types of investments (e.g., privately held investments) from being eligible to be purchased with IRA money; or

- Correct or clarify the manner in which the 10-Year Rule created by the original SECURE Act should be implemented for Non-Eligible Designated Beneficiaries.

There are many complexities to the Secure Act 2.0 and we will continue to keep you abreast of all that it entails and ensure you are adhering to it. There are now more dates, rules and numbers to keep track of and we will make sure you are in compliance with all of it.

This commentary reflects the personal opinions, viewpoints and analyses of the Seaside Wealth Management, Inc. employees providing such comments, and should not be regarded as a description of advisory services provided by Seaside Wealth Management, Inc. or performance returns of any Seaside Wealth Management, Inc. client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Seaside Wealth Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Read More

How Often Should I Meet With My Financial Advisor?

Retirement Withdrawal Strategies: How to Make Your Portfolio Last in Retirement

Mid-Year Check-Up for Retirees: Ensure You Don’t Run Out of Money

Use Your Old 529 Plan to Fund a Roth IRA for Your Kids

Is Social Security Going Bankrupt?