Total Return vs Income Investing in Retirement

In order to beat inflation should you invest for income or for total return?

With inflation at the highest levels we have seen in 40 years, you may be wondering whether you should devote more of your portfolio to dividend paying stocks. A dividend is the distribution of some of a company's earnings to a class of its shareholders (click here to learn more) typically in the form of cash. You may also be wondering if you should invest in things that pay a higher income in order to overcome inflation.

This may be tempting, especially if you are in or near retirement. The challenging thing about retirement is that you must replace your paycheck with an income stream that needs to rise throughout a 30 (plus) year retirement. To go from a steady income stream to now depending on taking income out of your investment portfolio can be tricky, especially if your investments are moving all over the place because of market volatility. In addition, factors such as creating income in a tax-efficient manner come into play as well. We get asked all the time about whether a retiree should invest to maximize the income generated from their portfolio or whether they should take a different approach.

Let’s begin by defining the two sources of investment returns:

- Capital appreciation is an increase in the value of the investment itself.

- Income (or “yield”) represents payments made to the investor during the holding period, such as dividends in the case of stocks, or coupon payments for bonds.

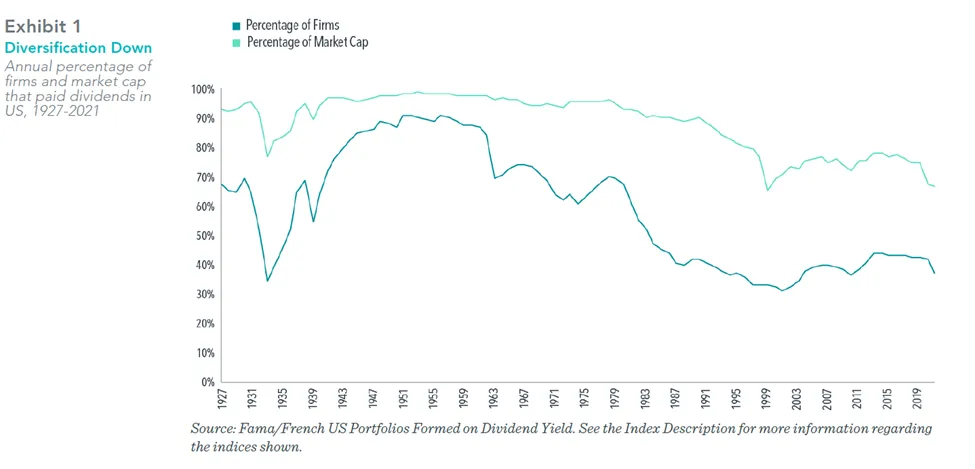

Before diving into the performance of dividend paying stocks it’s important to note that the number of companies paying dividends has declined to only 38% of firms in 2021. This means that if you chase dividend paying companies you will be sacrificing diversification since you will own so many fewer names. In addition, a dividend focused strategy does not necessarily provide stable income. In fact, changes in dividend policy are common, especially during times of higher uncertainty. For example, many dividend payers cut their dividends during the pandemic in the first three quarters of 2020, dividends from each dollar invested in US markets decreased by 22% compared to the same period in 2019.

Do dividends combat high inflation?

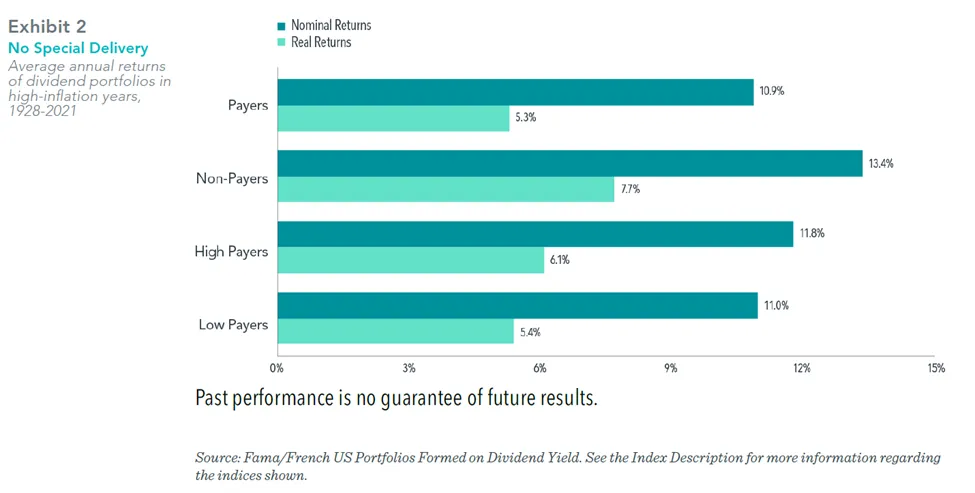

We studied four groups of stocks: high dividend payers, average dividend payers, low dividend payers and companies that pay no dividends. We found that all four groups of stocks outpaced inflation but surprisingly, the companies who paid no dividends at all actually outperformed.

Do Dividend paying stocks outperform when the Federal Reserve raises interest rates?

We studied time periods when the Federal Reserve increases interest rates and found no clear outperformance of dividend paying stocks during time periods such as these. There’s no strong evidence that dividend stocks have delivered superior inflation-adjusted performance during periods of high inflation or rising interest rates.

Do high yield bonds provide more income?

Bonds with longer maturities and lower credit quality generate higher yields, leading some investors to allocate more to these segments of the bond market. Longer-dated bonds, however, are more interest-rate sensitive, and lower-rated bonds tend to be more correlated to stock market movements, especially in times of crisis, making these categories of bonds more volatile. While adding high-yield bonds to the portfolio can potentially generate higher returns, they come with significantly more volatility and risk to the portfolio. While adding these higher yielding segments to a portfolio can have certain benefits, we would caution against adding them simply to increase yield. Furthermore, bonds are typically used to provide a buffer against the volatility of the stock portion of the portfolio; introducing additional risk on the bond portfolio diminishes its ability to do so.

What is a total return approach?

A total return approach considers both capital appreciation (growth) as well as dividends and blends both styles into the “best of both world approach.” In contrast to traditional income strategies, the total-return approach generates income from capital gains in addition to portfolio yield. This approach begins with building a diversified portfolio matched to an investor’s risk tolerance. There are several advantages of this way of investing:

- Portfolio diversification. Total return strategies are more diversified across many different asset classes. Income generating strategies can end up too concentrated in fewer names or asset classes and this adds risk to the portfolio. Diversified portfolios tend to be less volatile and hold up better during stock market shocks.

- Tax efficiency. Since a portion of investors income comes from capital gains this results in a lower tax liability as capital gains are taxed at lower rates than ordinary income for most retirees.

- More control over the size and timing of portfolio withdrawals. With a total return strategy, investors may have more peace of mind because they can spend from capital gains in addition to portfolio yield. Numerous studies suggest that if you follow a disciplined withdrawal plan under a total-return strategy, your savings could last years.

Given everything we have discussed, reaching for yield comes with a variety of risks and negative consequences. A total return approach can help to minimize portfolio risks and maintain portfolio longevity while enabling investors to reach their goals and bring their financial plan to life.

Many investors seeking income would be better served if they adopted a total return strategy that spends through capital returns in addition to portfolio income yield.

Read More

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

How Often Should I Meet With My Financial Advisor?

Smart Money Moves to Make for 2026

26 Things To Consider In 2026