U.S. Presidential Election: What does it mean for your Financial Plan and Investments?

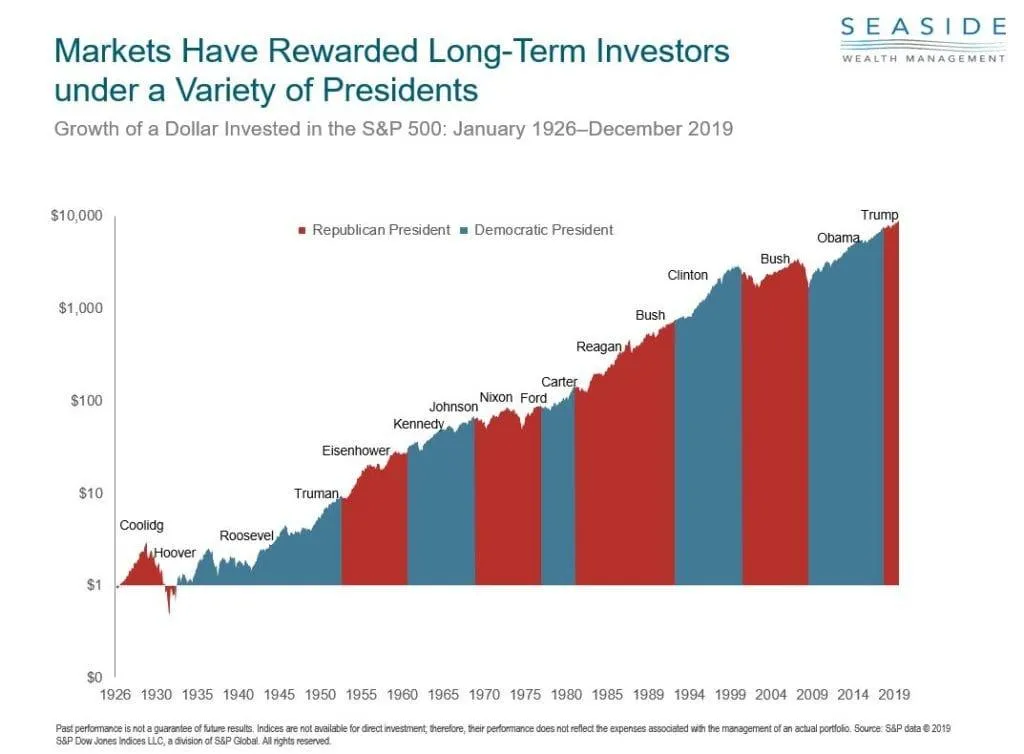

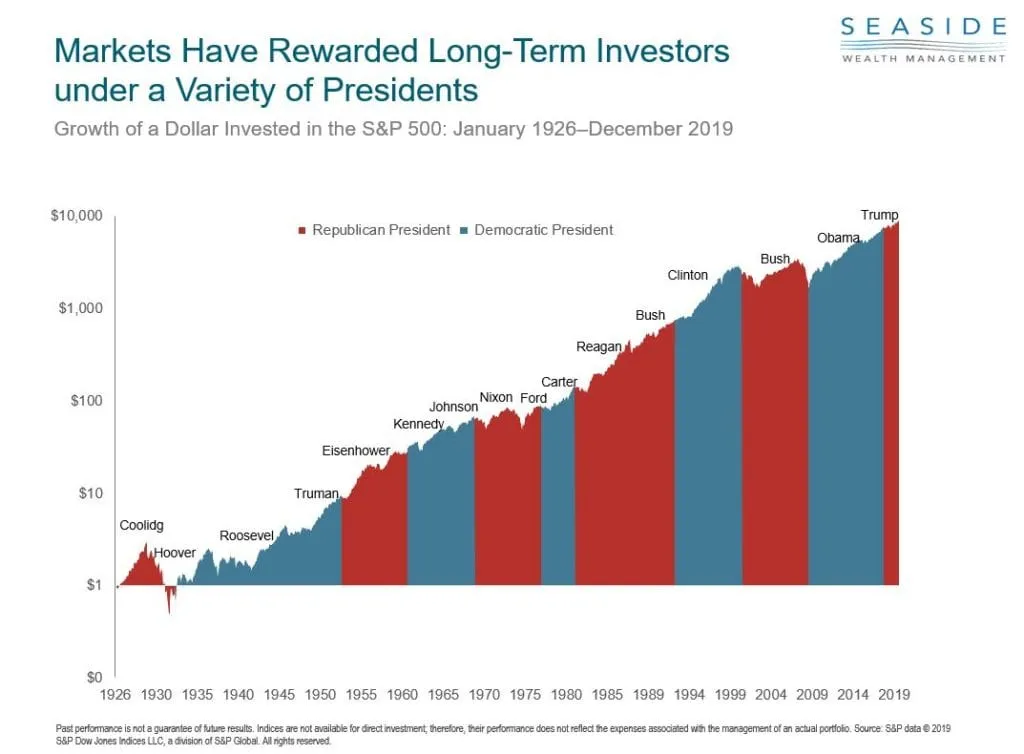

As I write this, a winner in the 2020 U.S. Presidential election has not been declared and a bitterly contentious, hard-fought battle for the Oval Office ensues. But one thing we know for certain is that the U.S. stock market is bigger than any one person or one political party as evidenced by the historical growth of $1 during a variety of Presidential terms. It is important to stay focused on your longer-term goals and the bigger picture and not the short-term market adjustments.

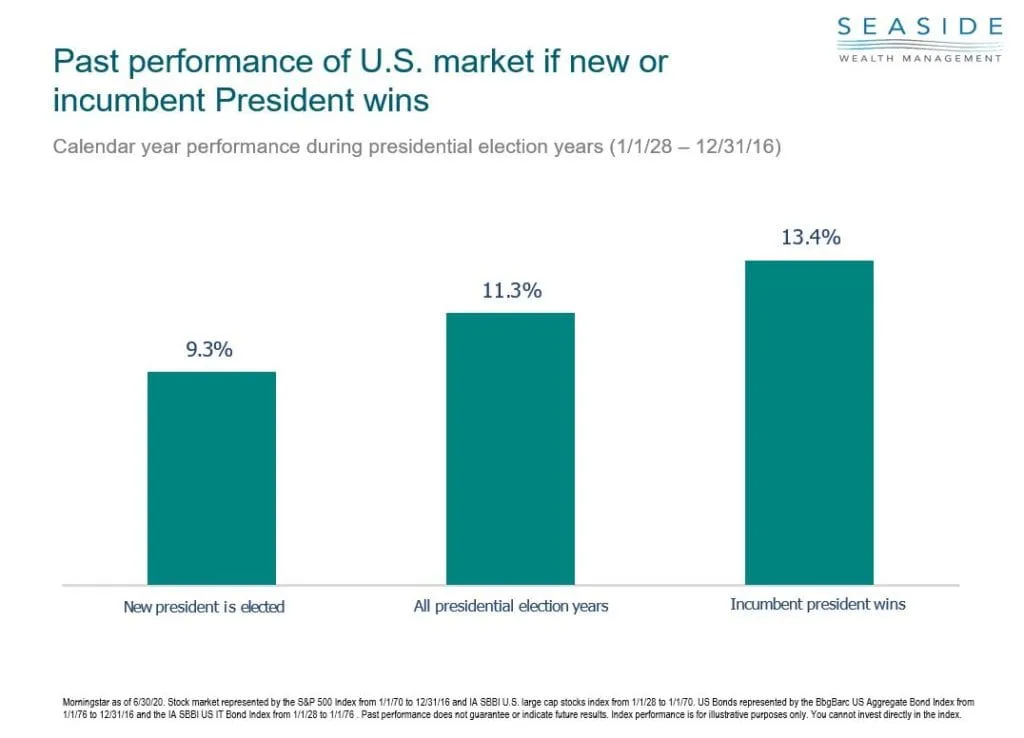

Since history tends to repeat itself, a Biden or Trump victory should be mostly “noise” to stock market valuations. While it may seem like a very emotional time right now for many reasons, the stock market tends to do well despite who is in office. In addition, since 1928, the stock market has gone up whether a new president has won or the incumbent was victorious (see below).

Since we can’t control the outcome of the election nor the market’s reaction to it, the most prudent thing to do is explore the strategies, planning opportunities and tactics that present themselves as a result of a victory of either candidate. Since Joe Biden has more confirmed electoral votes at the moment, we will start with his plans:.

Let’s examine the tax agenda that President Biden has proposed while on the campaign trail:

- An increase in the corporate tax rate from 21% to 28%

- Raising the top income tax rate on regular income back to 39.6% from 37%

- Ending the step-up basis at death

- Treating long-term capital gains and qualified dividends as regular income for those earning over $1 million

- Applying the Social Security payroll tax on incomes over $400,000+

We believe that lifting the top income tax rate back to 39.6% may possibly hinder economic growth, but the effect would be small. You may recall that this top marginal tax bracket existed under President Clinton and in President Obama’s second term and no recession happened in either period.

On raising the corporate rate to 28%, I suggest looking at the glass as half-full. Did anyone seriously believe the corporate rate would stay this low forever? The corporate tax rate remained at 35% from the early 1990s all the way through 2017. Furthermore, we have not seen a corporate tax rate as low as 21% since the 1930s! The market is a discounting machine, meaning that if Democrats take back power and only raise corporate tax rates to 28%, that’s considered a “win” in a way, because it means future policy debates on the corporate tax rate will range from, say 21% to 28%, not back up to 35%.

In addition, eliminating the step-up basis at death would be an administrative nightmare for some heirs who inherit assets with no records of when the assets were originally bought or at what price. Rememberthat tracking cost basis electronically has only existed for the last several decades. Many of these heirs are far from wealthy themselves and would find it challenging to pay for this potential astronomical tax levy. More likely, the Senate would reduce the exemption amounts for the estate tax, instead (currently you can pass $11,580,000 tax free to your heirs and an unlimited amount to your spouse).

More troublesome from an economic growth perspective would be treating capital gains and qualified dividends as regular income for those making $1 million or more. For dividends, this would unravel about twenty years of tax policy reducing the double-taxation on dividends (monies are taxed when a company earns profits and then again at the personal level). On long-term capital gains, the tax rate hasn’t been as high as 39.6% since the early years of the Carter Administration. That’s right, even Jimmy Carter thought that tax rate was too high!

Raising the rate to this level would be a major disincentive for investors. Given that the economy will be far from fully healed in 2021, we have serious doubts the Biden Administration could rally relatively moderate Democrats to such a tax hike. Remember, President Obama had 59 (and then 60) Senate votes and a large majority in the House when he became president in 2009, yet the Bush tax cuts he inherited were not unwound until 2013, and then, only partially.

The most aggressive idea that Biden has proposed would be to impose the Social Security tax on regular earnings above $400,000. At present, that tax – 6.2% on workers, 6.2% on employers – applies only on the ‘wage base” up to $137,700 in 2020, with the wage base going up each year based on wage growth.

Imposing an extra 12.4% tax would be a large disincentive for high-income workers. Tack that on top of the official 39.6% income tax rate, plus the 2.9% Medicare tax, and we’re at more than 50% (our math is factoring-in that some of the cost is paid by the employer, but the cost is ultimately borne by the worker). Then add in a top tax rate of 13.3% for California, which may be going higher, and you have net marginal tax rates nearing 65%. We think it is unlikely that the Biden Administration would be able to impose this extra layer of payroll tax. The special budget rules in the U.S. Senate do not apply to any aspect of Social Security: not benefits and not taxes. Changing any aspect of Social Security requires going through “regular order” in the Senate, which means the proposal could be filibustered until it gets 60 Senators willing to support it. The odds of that are low.

The bottom line is that a Biden win coupled with Democrats winning the Senate would mean taxes would go up. At this point, we don’t think they’d be raised fast enough or high enough to generate a recession by themselves More likely, it means that that after an early spurt of growth this year and perhaps into next year as the economy heals from the COVID-19 disaster, we’d be more likely to settle into a moderate to slow pace of economic growth like we had in 2009-2016, rather than the somewhat faster pace of 2017-2019.

Under President Trump, taxes are likely to remain low. He has promised a middle-class tax cut, reduced taxes on capital gains and continued regulatory relief. He is likely to continue aggressive trade policies including tariffs and he has threatened to punish China for failing to contain the coronavirus.

One similarity is that both candidates have pledged a massive, multitrillion-dollar coronavirus relief bill. Biden’s proposal could top $3.4 trillion and include an infrastructure package and billions of dollars for state and local governments. Trump’s most recent stimulus plan was worth $1.8 trillion. He recently said he was willing to “go big,” suggesting he was open to more funding that could put him at odds with the GOP.

In either case, Wall Street is betting on another stimulus package from whoever wins the election. Whichever party wins, the White House and Congress are likely to approve another stimulus package, the COVID-19 vaccine will be available within the next year and the U.S. economy is recovering, slowly but surely.

With the additional stimulus comes the possibility of a weakening U.S. dollar which has been very strong over the last decade. A weakening U.S. dollar will help to improve returns of international investments as foreign profits are brought home to a dollar that is not as strong as the currency the profits were earned in. A softening U.S. dollar is typically a tailwind for international investments. For the last decade the opposite has been true as a strong U.S. dollar reduced international equity returns. This is a great reminder that diversification (including domestic and international investments) is a prudent way to build an all-weather portfolio. While U.S. investments have outperformed their international counterparts recently, the tide may be turning as it often does from time to time.

One final thing to keep in mind: one election does not make or break a nation. Before long, the 2022 mid-terms will loom large and the presidential election in 2024 will be upon us, with the American people ready to render electoral verdicts and make adjustments again and again.

Read More

5 Retirement Investment Strategies for Modern Longevity

How the Right Retirement Planning Services Determine Whether Your Savings Last

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Outdated Estate Planning Can Cost The Family It Was Meant To Protect

How Social Security Timing Can Make A $600K Difference in Taxes