Breaking News – Tax Changes Coming

Last week the House Ways and Mean Committee released a bill detailing some changes to the tax code. We have been watching these events very closely and wanted to bring you an update. While the law is not in its final form, we wanted to make you aware of some of the potential changes we need to be prepared for.

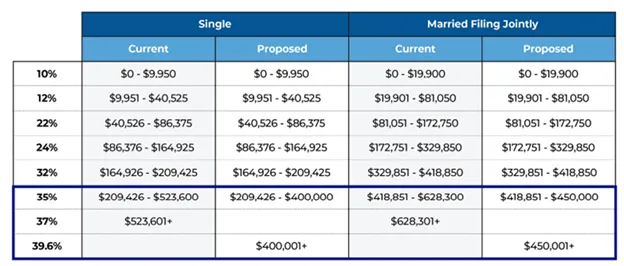

The top tax rate will increase to 39.6% on high earners. The top tax rate had been at 39.6% from 2013 through 2017. It was reduced to 37% beginning in 2018 with the enactment of the Tax Cuts and Jobs Act of 2017. If enacted, the current bill would reinstall 39.6% as the top ordinary income tax rate, beginning in 2022. Currently, top tax rates are at 37% and start at $523,600 for single filers and $628,300 for married filers. The new law will not only increase top marginal brackets, but will also lower the amount of income required to reach them to $400,000 for single filers and $450,000 for married filers.

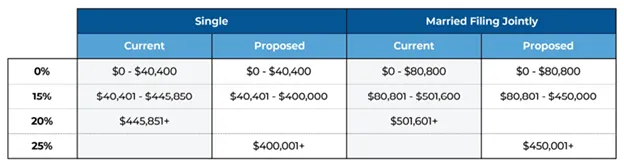

In addition, there will be a 3% ‘surtax’ on income above $5MM. Long term capital gains rates will increase to 25% and this change will take place immediately, effective September 14, 2021.

The proposal also aligns the income threshold for the top long-term capital gains rate with the income threshold for the top ordinary income tax rate. So, the top long-term capital gains rate of 25% will take effect at the same threshold ($400,000 for single filers, $450,000 for married filing jointly), at which point the 35% ordinary income tax bracket would become the 39.6% ordinary income tax bracket.

The Step-Up in Basis Will Remain

One piece of good news is that the Step-up in basis will remain. When someone dies, the cost basis of their non-retirement assets gets stepped-up to current market valuations. This effectively allows your heirs to sell those assets tax free. Highly appreciated real estate and stocks, mutual funds and ETFs can be sold by your kids and heirs allowing them to enjoy the total amount of the proceeds tax free.

Several planning techniques and strategies will be going away

Backdoor Roth Strategy Going Away

The new law cracks down on some of my favorite planning techniques that we have been using for years. I have always thought these so-called loopholes would be going away and unfortunately, it turns out I was right. The new legislation will be disallowing Roth conversions on after-tax dollars. Effectively, this is the end of the backdoor Roth strategy.

Roth Conversions going Away

Effective January 1, 2022, the ability to convert a traditional IRA to a Roth IRA will be going away. There is one exception, however. For high income earners the ability to convert a traditional IRA to a Roth IRA will be going away but not immediately. The prohibition on conversions for high-income taxpayers would not take effect until 2032.

I think the reason they are allowing conversions for high income earners for 10 more years is because this will continue to generate revenue in the form of taxes for 10 additional years. Budget projections typically go out 10 years. Legislators want to be able to count on that income for a while longer.

The Mega Backdoor Roth Strategy is going away

One of my favorite planning techniques is the so-called Mega Backdoor Roth strategy. This is where you can contribute to an after tax 401(k) and then convert it to a Roth IRA. This can be sometimes while working, and sometimes after leaving your employer depending upon the plan’s rules. This strategy will be eliminated by the new legislation.

Application of the 3.8% Net Investment Income Tax (NIIT) To High-Income S Corporation Owners

Under current law, profits of S corporations are not subject to employment taxes (e.g., FICA taxes, Self-Employment Tax), or the Net Investment Income Tax (NIIT). If enacted, the proposal would change that for certain high-income S corporation owners. Once an S Corporation’s Modified Adjusted Gross Income reaches certain thresholds, their profits will be subjected to additional tax the bill is calling Specified Net Income tax.

The applicable thresholds are as follows:

- Single filers – $400,000

- Joint filers – $500,000

New 3% Surtax for Ultra-High-Income Taxpayers

The new bill would add a new 3% surtax on ultra-high-income taxpayers. The new surtax would apply to individual taxpayers when their MAGI exceed $5 million. While this may sound like a lot of money, certain events could trigger this amount such as the sale of a large property or a business. The $5 million threshold will apply to both single and joint filers.

The 3% surcharge will apply to trusts income in excess of $100,000. And, while given today’s low-rate environment (requiring a substantial amount of assets to generate $100,000 of income via interest and dividends), capital gains would also be subject to the surtax.

Furthermore, to the extent a trust is the beneficiary of a retirement account, it may receive substantial amounts of income annually in the form of distributions from the account (especially when the new 10-Year Rule created by the SECURE Act applies!).

New Required Minimum Distributions for Taxpayers With High Income And Mega-Sized Retirement Accounts

If a taxpayer has both 1) high income, ($400,000 for single filers, $450,000 for joint filers); and 2) total retirement accounts worth more than $10 million, they will be subject to Required Minimum Distributions for the year.

Such distributions would be required regardless of the age of the account owner. For young owners (under age 59 ½) of mega-retirement accounts with high income, the law does provide one welcome benefit. The 10% early distribution penalty will not apply to amounts distributed due to this new requirement. The distributions will still be fully taxable.

For individuals with between $10 million and $20 million in total retirement accounts, the amount of the RMD would be equal to 50% of total retirement account dollars in excess of $10 million.

Special Rule For Roth IRAs With High Income And Total Retirement Account Balances In Excess Of $20 Million

In general, Roth IRAs are not subject to Required Minimum Distributions during an individual’s lifetime. That would change, however, for high-income (as defined above) Roth IRA owners with total retirement account balances in excess of $20 million.

The rules around this are a bit confusing so stay tuned for further clarification as it comes out and to the extent this becomes law.

Restrictions on New IRA Contributions for Taxpayers with High Income and Mega-Sized Retirement Accounts

Along with requirements to take RMDs from large retirement accounts, the new bill will also prevent high income earners and mega-sized retirement accounts from making any new IRA contributions. Beginning in 2022, in any year where you have taxable income above $400,000 for single filers and $450,000 for MFJ and your total retirement accounts are worth more than $10 million, you will be prohibited from making an IRA contribution. It’s worth noting that this prohibition does not apply to employer sponsored retirement plans like 401(k)’s.

The Qualified Business Income Deduction is Capped

While the QBI deduction will not be eliminated, it will be capped for high income earners (taxpayers with income in excess of $400,000). The bill would simply cap the maximum amount of the deduction a taxpayer can claim. The maximum allowable income for QBI deductions would be as follows:

- Single filers – $400,000

- Joint filers – $500,000

- Trusts and estates – $10,000

So, the QBI deduction is not going away. Once the deduction reaches the maximum amount, additional amounts will be disregarded.

Bottom Line

The new law is still pending there may be some changes to the initial proposal. We will continue to monitor the situation and keep you aware of what the final bill looks like. Additionally, you can count on us to continue to research strategies and methods to help you save money on taxes after the legislation passes. In the interim, please feel free to reach out to our office with any questions or concerns you may have.

Read More

5 Roth IRA Conversion Strategies To Prevent Six Figures In Taxes

The Truth About Tax-Free Retirement

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

How Often Should I Meet With My Financial Advisor?