Should I Retire Early?

Retiring early is a common dream for many, but the decision to do so can be a difficult one. Having every day off to do what you want sounds appealing, especially when work is getting tiring. However, one mistake can derail a lifetime of good planning, saving and investing. The risks associated with retiring early should be considered in light of the potential rewards that come with such a decision. Ultimately, the success of a decision to retire early will depend on your financial security and preparedness for the lifestyle change.

One risk associated with retiring early is that you will not have access to medical insurance once you leave your employer. Purchasing your own health insurance can be expensive, sometimes costing upwards of $1,500 per person each month. You can consider going on COBRA but this will only last 18 months and is quite expensive. Make sure to have a line item in your budget for medical insurance to cover the gap between retirement and Medicare eligibility at age 65.

Another risk with retiring early is that you may burn through your savings more quickly than expected. The financial security you had planned for may not last as long as you had initially thought, resulting in a need to find additional sources of income. Without the ability to generate steady income through a job, you may not be able to maintain your desired lifestyle. Ideally, you will delay Social Security as long as possible and let it increase by 8% per year. In order to successfully delay Social Security, you need to have enough cash or investments to sustain an increased distribution while delaying.

Additionally, there is the risk of becoming bored with retirement. Without the structure and social interaction of a job, you may become restless and unfulfilled. Unless you can find ways to occupy yourself, such as hobbies or volunteer work, you may quickly become unsatisfied with your decision to retire early. Finding meaning, passion and purpose are very important to the retirement planning process and are often overlooked. People tend to focus on the financial aspects of retirement and ignore the important piece about what they want to do when everyday’s like a Saturday. Finding purpose should be your top priority. Until then, don’t even think about retiring! We have seen it happen too many times where people will retire and don’t have anything to do. Depression in retirement is a very real thing and can be avoided with some proper planning and thoughtful insight.

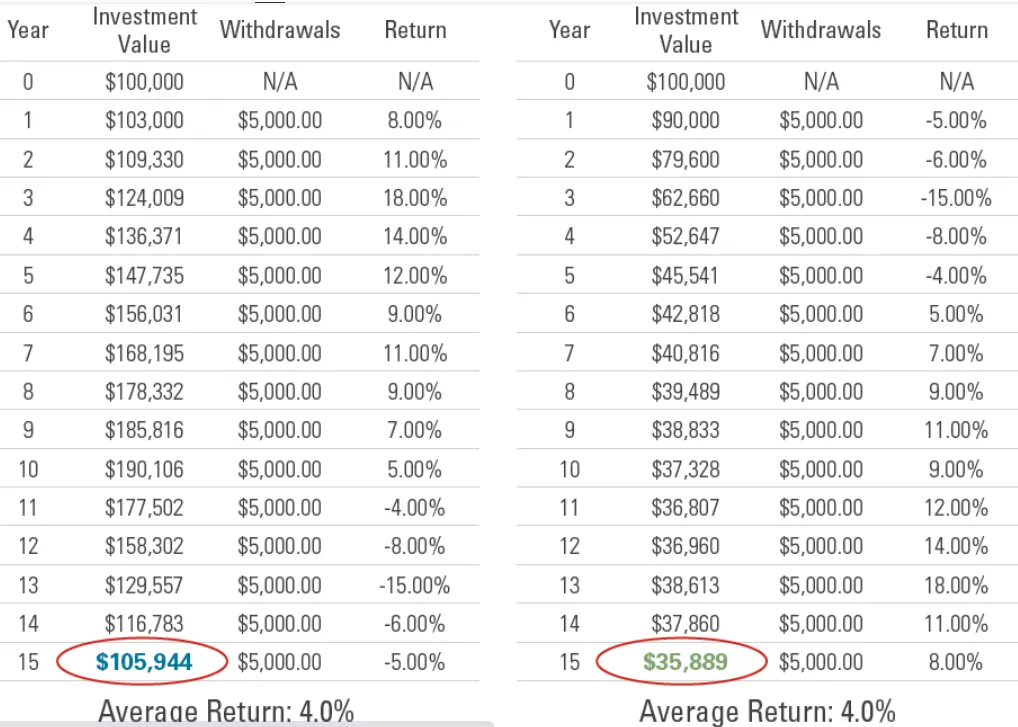

Finally, there is the “Sequence of return risk” of the markets having a string of bad years resulting in your portfolio being spent down too quickly. In such a situation, your financial security may be jeopardized, and your decision to retire early could become a costly one. This happened to people who retired in 2000 at the height of the dot com bubble. The following 3-year market meltdown known as the “tech wreck” sent many retirees back to work as they saw their nest egg get cut in half over a 3-year period. If bad returns happen early in retirement this could result in a negative outcome for you.

There are two hypothetical charts depicting potential sequences of returns during your first 15 years of retirement. The chart on the left shows a more normal distribution of annual returns and the value of your investments would be at about the same level after 15 years. The chart on the left shows the impact of several years of a down market at the outset of your retirement. As you can see these early negative returns would serve to substantially deplete your retirement after 15 years, putting your retirement financial security at risk.

Additionally, you may live a lot longer than you are planning on resulting in the risk that you may outlive your retirement savings. People are living into their mid 90’s and in some cases beyond that. It’s imperative that you take this into consideration as you are thinking about your own retirement planning. Retirement can very easily last four decades and you need to create a rising income stream to outpace inflation for a very long time.

Early retirement is not an all or nothing proposition. It is very common for people to phase into retirement. This could mean reduced hours at your current employer or perhaps becoming a consultant in your field. For some it means a career switch into an “encore career.” This could entail starting a business or something else.

If this is an option for you it could also help you transition into retirement financially and emotionally. A reduced work schedule can help you experiment with non-work ways to spend your time. Perhaps this is golf, traveling or volunteering. On the financial side this is a chance to adjust your spending to a retirement budget on a gradual basis.

In conclusion, while there are risks associated with retiring early, they can be mitigated with thorough financial planning. You should determine whether you will have enough money saved to last throughout retirement, and research the particular benefits associated with your retirement plan. Make sure to properly stress test your plan to ensure it will hold up no matter what the market throws at you. With the proper planning and preparation, retiring early can be an exciting and rewarding experience.

Follow us on social media for videos, blogs, and market updates!

This commentary reflects the personal opinions, viewpoints and analyses of the Seaside Wealth Management, Inc. employees providing such comments, and should not be regarded as a description of advisory services provided by Seaside Wealth Management, Inc. or performance returns of any Seaside Wealth Management, Inc. client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Seaside Wealth Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Read More

How to Structure Retirement Income Planning for Modern Life Expectancy

Why Your CPA and Financial Advisor Should Be Best Friends

How Often Should I Meet With My Financial Advisor?

Smart Money Moves to Make for 2026

26 Things To Consider In 2026