Understanding How Your Social Security Benefits Are Taxed

As you approach retirement age, it is crucial to have a comprehensive understanding of how your benefits will be taxed. Social security taxes can be complex and confusing, but with the right knowledge, we can help you make informed decisions to minimize them. In this article, we will demystify social security taxes and explore how they affect both retirees and working individuals.

How Are Social Security Benefits Taxed?

Before we delve into the specifics, let's first understand how social security benefits are taxed. The taxation of these benefits is based on your combined income, or “provisional income” as it is sometimes referred to. Your combined income includes your adjusted gross income (AGI), nontaxable interest (like muni-bond interest), and one-half of your social security benefits. The Internal Revenue Service (IRS) has a formula to determine the taxable portion of your benefits.

Understanding the Taxation of Social Security for Retirees

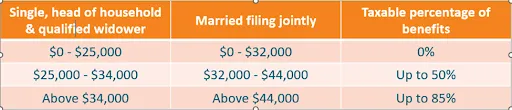

Retirees often rely on social security benefits as a significant source of income. However, it is important to note that not all retirees will face taxation on their benefits. The taxation depends on your combined income. If your combined income is below a certain threshold, your benefits will not be taxed at all. However, if your combined income exceeds the threshold, up to 85% of your benefits may be subject to taxation.

Take a look at the chart below to get a sense for what this looks like:

To calculate your combined income, you need to add up your adjusted gross income, nontaxable interest, and half of your social security benefits. It is essential to keep track of these numbers and consult with a tax professional to determine the exact amount of your taxable benefits.

Taxation of Social Security for Working Individuals

For individuals who continue to work while receiving social security benefits, the taxation can become even more complicated. If you are under the full retirement age, there is an earnings limit imposed by the Social Security Administration (SSA). If you earn more than this limit, a portion of your benefits may be temporarily withheld.

In 2023, the earnings limit is $21,240. If you reach full retirement age in 2023, the limit on your earnings for the months before full retirement is $56,520.

Once you reach the full retirement age, there is no longer an earnings limit, and you can receive your full benefits regardless of your income. However, it is important to remember that your benefits may still be subject to taxation based on your combined income.

How to Calculate the Taxable Portion of Your Social Security Benefits

Now that you understand the factors that contribute to the taxation of social security benefits, let's explore how to calculate the taxable portion. The IRS provides a worksheet that helps you calculate the exact amount of your benefits that will be subject to taxation.

To use the worksheet, you need to know your adjusted gross income, nontaxable interest, and the total amount of your social security benefits. By following the instructions provided, you can determine the percentage of your benefits that will be taxable.

Strategies to Minimize the Impact of Social Security Taxes

While we may not have complete control over the taxation of our social security benefits, there are strategies we can employ to minimize their impact. One such strategy is to carefully manage other sources of retirement income. By strategically withdrawing funds from different accounts, you can potentially keep your combined income below the taxation thresholds, thereby reducing the taxable portion of your benefits.

Roth IRA’s, in particular, are good sources to make tax free distributions from. Money coming out of a Roth IRA does not count towards your provisional income and therefore does not increase the taxes you pay on your social security benefit.

If you do not have a lot of money in your Roth IRA you can consider a Roth conversion strategy during your “gap years”.

Another strategy is to consider delaying your social security benefits. By delaying the start of your benefits, you can increase the amount you receive each month. Additionally, by delaying the benefit, this keeps your income lower allowing you to do more Roth conversions during the gap years, ultimately resulting in you paying less taxes on your social security benefit in the future.

This is all part of a combined strategy to maximize your Social Security income while lowering your tax bill in retirement.

Common Misconceptions About Social Security Taxes

There are several common misconceptions surrounding social security taxes. One of the most prevalent misconceptions is that if you pay taxes on your income, you will not have to pay taxes on your social security benefits. However, as we have discussed, the taxation of social security benefits is determined by your combined income, which includes other factors besides your income tax liability.

Another misconception is that once you start receiving social security benefits, the taxation remains constant. In reality, the taxable portion of your benefits can change from year to year depending on your income. It is essential to review and adjust your tax planning strategies accordingly.

Planning for Social Security Taxes in Retirement

Given the complexities of social security taxes, it is crucial to include them in your retirement planning. By having a comprehensive understanding of how your benefits will be taxed, you can make informed decisions about other sources of income, timing of benefit withdrawals, and potential strategies to minimize taxes.

Resources for Further Information on Social Security Taxes

To further educate yourself on social security taxes, there are several resources available. The Social Security Administration website provides detailed information on the taxation of benefits, including publications and interactive tools. The IRS website also offers publications and forms related to social security taxes.

Conclusion

Understanding how your social security benefits are taxed is essential for effective retirement planning. By familiarizing yourself with the factors that contribute to the taxation of benefits and exploring strategies to minimize their impact, you can make informed decisions to maximize your retirement income. Remember to consult with professionals and utilize available resources to maximize your benefits and reduce your tax liability.

This commentary reflects the personal opinions, viewpoints and analyses of the Seaside Wealth Management, Inc. employees providing such comments, and should not be regarded as a description of advisory services provided by Seaside Wealth Management, Inc. or performance returns of any Seaside Wealth Management, Inc. client. The views reflected in the commentary are subject to change at any time without notice. Nothing in this commentary constitutes investment advice, performance data or any recommendation that any particular security, portfolio of securities, transaction or investment strategy is suitable for any specific person. Any mention of a particular security and related performance data is not a recommendation to buy or sell that security. Seaside Wealth Management, Inc. manages its clients’ accounts using a variety of investment techniques and strategies, which are not necessarily discussed in the commentary. Investments in securities involve the risk of loss. Past performance is no guarantee of future results.

Read More

Why $1 of Extra Income Can Cost You $5,000 In Retirement Tax Planning

How Social Security Timing Can Make A $600K Difference in Taxes

7 Gift Tax Strategies for Helping Adult Children Without Ruining Your Retirement

5 Roth IRA Conversion Strategies To Prevent Six Figures In Taxes

The Truth About Tax-Free Retirement